- Currency Finance (formerly Currency Capital) is an equipment financing marketplace — not a direct lender — that connects borrowers with 30+ lending partners for equipment loans and leases up to $500,000

- They finance just about anything with a motor or a hydraulic arm: excavators, tractors, semi-trucks, trailers, forklifts, CNC machines, medical equipment, restaurant equipment, and even aircraft

- The application is quick (minutes, not hours) and starts with a soft credit pull — but Currency publishes almost nothing about rates, fees, or qualification requirements on its website

- Terms run 2-6 years with no down payment required, and repayment options include monthly ACH or manual payments — but customer reviews warn about hidden prepayment structures despite the company claiming no penalties

- Best for: established businesses (2+ years) that need to finance specific equipment quickly, especially when buying through a dealer or auction site that already partners with Currency

What Currency Finance Actually Is

First, the name change. If you’ve been Googling “Currency Capital equipment loans” and getting confused, here’s the story. Currency Capital rebranded to Currency Finance a few years back. Same company, same ownership (it’s the financial technology arm of Sandhills Global, a media and technology company that runs heavy equipment marketplaces like Machinery Trader, Truck Paper, and AuctionTime). The website is now gocurrency.com. Old links to currencycapital.com should redirect.

And here’s the important part: Currency Finance isn’t lending you money. They’re a marketplace that sits between you and a network of 30+ lending partners. You apply through Currency, their platform matches your credit profile and equipment needs with appropriate lenders, and a lending partner actually funds the loan. Think of Currency as the matchmaker — they simplify the shopping process so you don’t have to call fifteen banks and fill out fifteen applications.

Why does that matter? Because the rates, fees, and terms you get aren’t set by Currency — they’re set by whichever lending partner picks up your deal. This explains why Currency’s website is maddeningly vague about specifics. They can’t tell you what rate you’ll get because they genuinely don’t know until a lender makes an offer. It also means your experience depends heavily on which partner you’re matched with, and that’s somewhat out of your control.

The Sandhills Global connection is actually a big deal, though most reviews don’t mention it. When you’re browsing excavators on Machinery Trader or trucks on Truck Paper and you click “Finance This Equipment,” you’re being routed to Currency. They’ve embedded financing directly into the equipment shopping experience. If you’re already on those platforms, Currency is the path of least resistance — which is exactly the point.

Currency Finance is integrated directly into equipment marketplaces like Machinery Trader and AuctionTime — click “Finance” and the application starts.

How Equipment Financing Through Currency Works

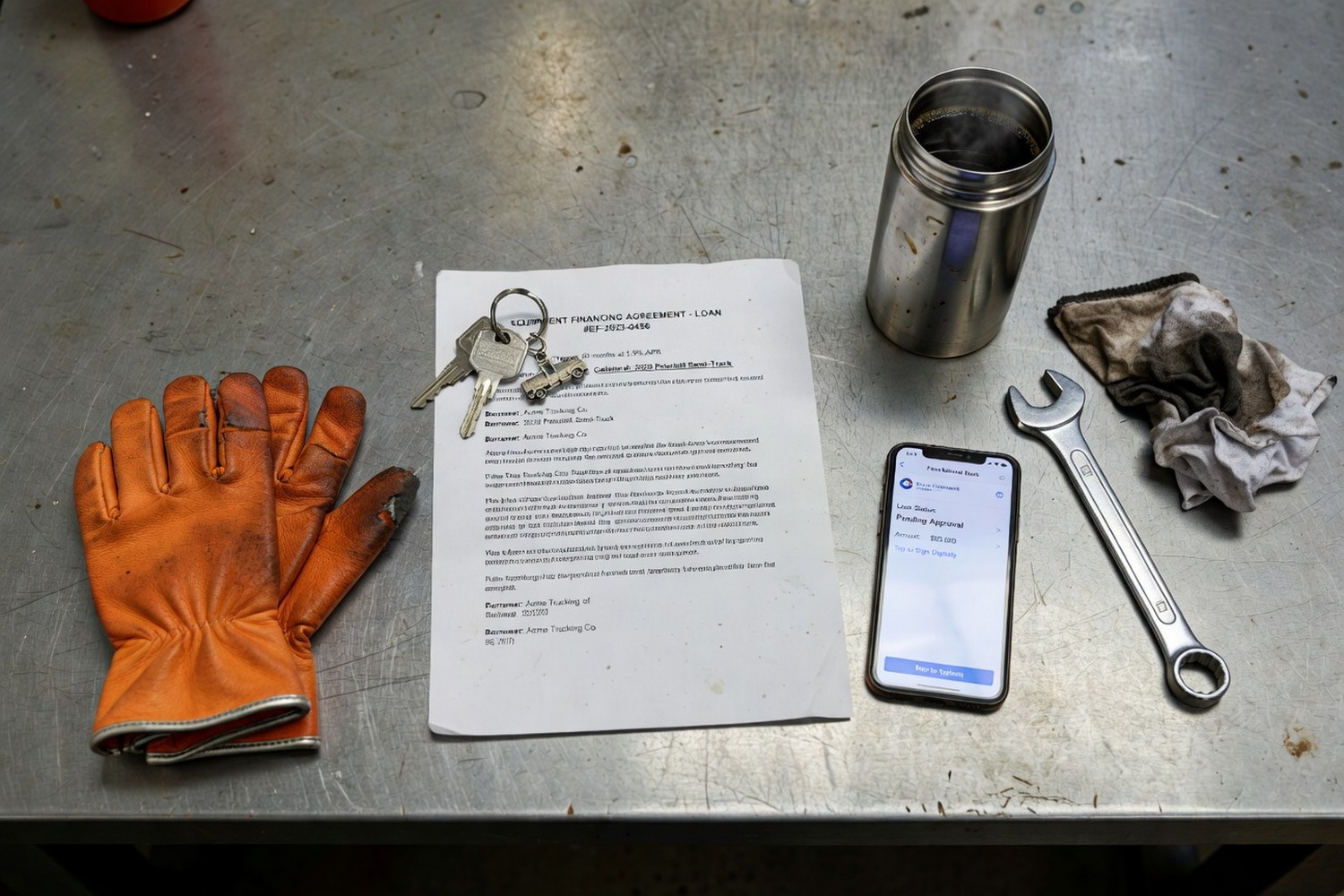

You find the equipment first. That’s the key difference between Currency and a general business lender. You’re not borrowing a lump sum to figure out later what to buy. You identify a specific piece of equipment — maybe a $120,000 excavator on AuctionTime, or a $45,000 box truck from a dealer — and then apply for financing for that specific purchase. Currency’s platform is built around the equipment, not around you.

The application is genuinely fast. Fill out the online form: business info, personal info, equipment details. Currency says it takes minutes, and that’s accurate based on user reports. They run a soft credit pull — no score impact — and match your profile against their lender network. You’ll hear back about preliminary approval quickly, sometimes the same day.

Then it gets lender-specific. Once a lending partner picks up your deal, they may request additional documentation: bank statements, proof of business ownership, tax forms showing how long you’ve been operating. The specific documents depend on the lender, the amount, and your credit profile. This is where the timeline stretches from “minutes” to “days” — the lender’s own underwriting process takes over.

Loan or lease — you choose. Currency’s lender partners offer both equipment loans (you own it at the end) and leases (you return it, upgrade, or buy it out). Leasing makes sense for equipment that depreciates fast or that you’ll only need temporarily. Loans make sense for long-lasting machinery you’ll use for years. Some lenders offer $1 buyout leases — essentially a loan structured as a lease for tax purposes.

No down payment required — which sounds great until you realize that zero-down means higher monthly payments and almost certainly higher rates. Some borrowers report better offers when they put 10-20% down, because it reduces the lender’s risk. If you have the cash, putting something down is usually the smarter financial move even if it’s not required.

Product Overview Table

| Feature | Details |

| Loan Type | Equipment loans and leases (marketplace model) |

| Max Amount | Up to $500,000 |

| Terms | 2-6 years |

| Interest Rates | Not disclosed (varies by lender partner) |

| Down Payment | Not required (but recommended) |

| Credit Pull | Soft pull initially, hard pull at formal application |

| Lending Partners | 30+ lenders in network |

| Equipment Types | Construction, farm, trucking, medical, restaurant, aircraft, and more |

| Prepayment Penalty | Company says no — but read the fine print (see Cons) |

Currency Finance does not publish rates or qualification minimums. All terms depend on the specific lending partner matched to your application.

What Equipment Can You Finance?

The list is genuinely broad — broader than most equipment lenders I’ve seen. Here’s what Currency’s platform covers, organized by industry:

Construction and heavy equipment: Excavators, bulldozers, backhoes, skid steers, cranes, compactors, concrete mixers. This is Currency’s bread and butter. Most of their lending partners specialize in heavy machinery, so the approval process for a $200,000 excavator is well-worn territory.

Trucking and transportation: Semi-trucks, flatbed trailers, dump trucks, refrigerated trailers, box trucks, utility vehicles. The Truck Paper integration makes this seamless — find a truck, click finance, fill out the form, get matched. Many owner-operators report using Currency for their first truck purchase.

Agriculture: Tractors (every major brand), combines, planters, sprayers, grain bins, irrigation systems. Through the Machinery Trader and AuctionTime platforms, Currency has deep ties to the ag equipment marketplace. Seasonal payment structures may be available through some lending partners.

Specialty and commercial: Medical equipment (MRI machines, dental chairs), restaurant equipment (commercial kitchens, walk-in coolers), manufacturing equipment (CNC machines, lathes, presses), forestry equipment, and — here’s the wild one — aircraft. Through their CurrencyAir division, they finance airplanes. Same platform, same process, just significantly more zeros on the loan amount.

Currency Finance handles everything from $15,000 utility trailers to $500,000 excavators — the equipment itself serves as collateral for the loan.

The Good and the Concerning

What works:

The marketplace model means one application reaches 30+ lenders — you’re not locked into one bank’s criteria. Equipment-specific expertise across every major industry. The Sandhills Global integration is genuinely convenient if you’re shopping on Machinery Trader, Truck Paper, or AuctionTime. No down payment option opens the door for businesses that can’t tie up cash upfront. Loan amounts up to $500K cover most equipment purchases. Both loan and lease options available. The initial soft credit pull means you can explore without committing. Customer service, when you get through to the right person, is generally praised in reviews — reps get name-checked positively on ConsumerAffairs.

What’s concerning:

Rate and fee opacity is the elephant in the room. Currency publishes nothing — not a rate range, not a fee schedule, not even a ballpark. You apply blind and hope the number that comes back is reasonable. Multiple ConsumerAffairs reviewers report discovering that their loan structure means they owe the full interest amount regardless of early payoff — directly contradicting Currency’s claim of “no prepayment penalties.” The fine print apparently requires you to pay the total of all scheduled payments even if you pay off the principal early. That’s not technically a “penalty,” but it achieves the same result: early payoff saves you nothing. Other reviews mention surprise fees, difficulty getting account statements, and poor communication after the loan closes. The pattern is familiar with marketplace lenders: the front end (application, approval) is smooth, and the back end (servicing, support, payoff) gets rough.

Who Gets Approved

Currency doesn’t publish qualification requirements — another frustrating gap on their website. Based on third-party reviews and lending industry norms for equipment financing, here’s what you’re likely looking at:

Credit score: Probably 575-625 minimum, depending on the lending partner. Equipment financing is generally easier to qualify for than unsecured loans because the equipment itself serves as collateral. If you default, the lender repossesses the excavator — that security means they’ll take more risk on credit score.

Time in business: Most likely 2+ years for the best terms. Some lending partners may work with newer businesses (1+ year) at higher rates. Startups are probably not getting approved unless they have strong personal credit and a substantial down payment.

Revenue: No published minimums, but the lender needs to see that your business can support the monthly payment. Equipment payments are typically 1.5-3% of the equipment value per month — so a $100,000 machine costs roughly $1,500-$3,000/month. Your revenue needs to comfortably support that on top of existing obligations.

Documentation: Expect to provide: 3 months of bank statements, proof of business ownership (articles of incorporation, EIN letter), personal identification, and details about the specific equipment you want to finance (year, make, model, seller information, purchase price). Some lenders may request tax returns for larger amounts.

The Application Process

Start at gocurrency.com — or click “Finance” on any equipment listing on Machinery Trader, Truck Paper, or AuctionTime. You’ll land on the same application form either way. Enter your business info (name, EIN, years in operation, revenue), personal info (name, SSN for soft pull), and equipment details (type, estimated price, dealer or seller). The whole thing takes 5-10 minutes.

Currency matches you with lenders. Their system runs your profile against the 30+ lender network and identifies which partners are likely to approve you. You’ll hear back — usually via phone call from a Currency rep — within a day or two. Sometimes faster if you’re a strong applicant for a straightforward purchase.

The lender takes over. Whichever partner picks up your deal will request additional docs, finalize terms, and present you with a loan or lease agreement. Read every page. Especially the prepayment section, the fee schedule, and the default provisions. If something is unclear, ask. If the rep can’t explain it clearly, that’s a red flag.

Funding and delivery. Once you sign, the lender funds the deal — usually paying the equipment seller or dealer directly. You don’t typically receive cash in your bank account. The equipment gets delivered (or you pick it up), and your monthly payments begin according to the schedule in your agreement.

Frequently Asked Questions

Is Currency Finance the same as Currency Capital?

Yes — same company, rebranded. Currency Capital became Currency Finance. It’s the fintech arm of Sandhills Global, which operates heavy equipment marketplaces like Machinery Trader and Truck Paper. The website is now gocurrency.com.

What interest rates does Currency Finance charge?

They don’t disclose rates publicly. Since Currency is a marketplace (not a direct lender), your rate comes from whichever lending partner is matched to your application. Rates vary based on credit, equipment type, amount, and term. The only way to find out is to apply.

Is there really no prepayment penalty?

Currency’s website says no prepayment penalties. However, multiple borrowers report loan structures where the total interest is owed regardless of early payoff — meaning you pay the same amount whether you keep the loan for 12 months or 48. Ask your specific lending partner about the payoff structure before signing.

What credit score do I need?

Not published, but equipment financing generally requires 575-625 minimum. The equipment serves as collateral, which makes approval easier than unsecured lending. Stronger credit scores get better rates and terms from the lending partners.

Can I finance used equipment?

Yes. Currency finances both new and used equipment through its lending partners. Used equipment may have age restrictions (some lenders cap at 10-15 years old) and lower maximum loan amounts, but it’s a core part of their platform — especially through AuctionTime and the used equipment marketplaces.

References

- SBA, “Equipment Financing Programs,” sba.gov

- FTC, “Understanding Vehicle Financing,” ftc.gov

- IRS, “Section 179 Deduction,” irs.gov

Keep Reading

- Best Small Business Loans: Compare Rates & Apply

- Construction Business Loans & Financing

- Food Truck Financing & Loans

- Best Long-Term Business Loans

- SBA Loans: Compare Programs

Rates and terms are subject to change. This is not financial advice. Currency Finance is a financial technology company and equipment financing marketplace, not a direct lender. Loan terms, rates, and requirements are determined by individual lending partners in Currency’s network. Always read the complete loan or lease agreement before signing, especially prepayment and fee provisions.